.jpg)

On 8 July 2025, the Reserve Bank of Australia (RBA) surprised many by keeping the cash rate steady at 3.85%, despite widespread expectations of a rate cut. Importantly, this decision revealed a split Board for the first time under Governor Michele Bullock, with six members voting to hold and three preferring a cut. The debate centred on "timing versus direction". This means interest rates are still likely to decrease, but the RBA wants stronger evidence of sustained inflation control before cutting again.

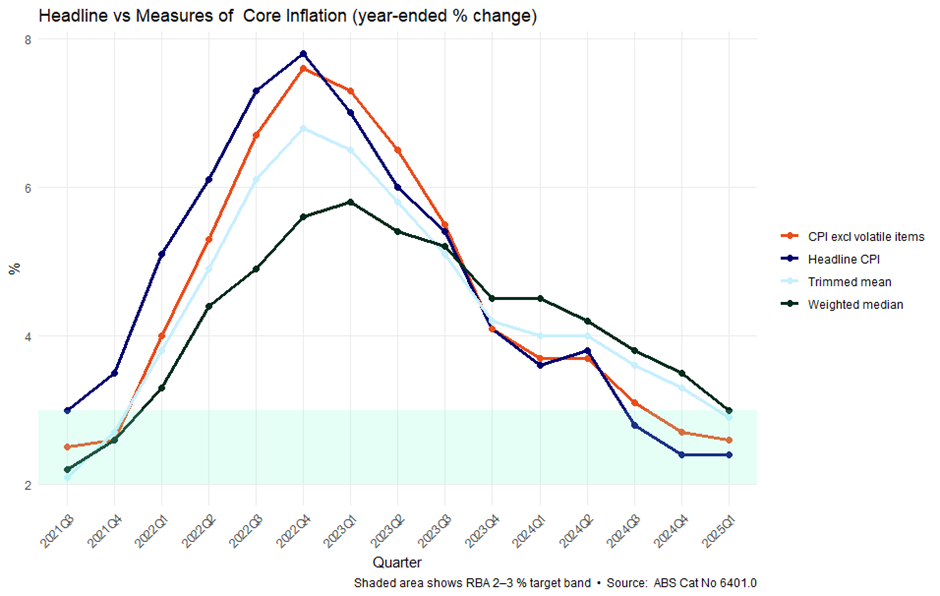

While headline CPI inflation eased back into the RBA’s 2-3 % target band at 2.4 %, driven partly by temporary energy rebates, the three core inflation measures (CPI excluding volatile items, weighted median, and trimmed mean) remain closer to 3 %. This indicates persistent underlying price pressures and prompted the RBA to maintain rates for now, aiming to ensure inflation consistently moves downward. The Board will therefore lean heavily on the June-quarter CPI (31 July) before acting, as cutting too early risks a costly policy reversal if inflation rebounds.

Board members who favoured a rate cut were concerned about soft economic signals and international risks, particularly new tariffs from the US. Overall, the RBA is prioritising caution to avoid needing future rate hikes, which could negatively impact homeowners and buyers alike.

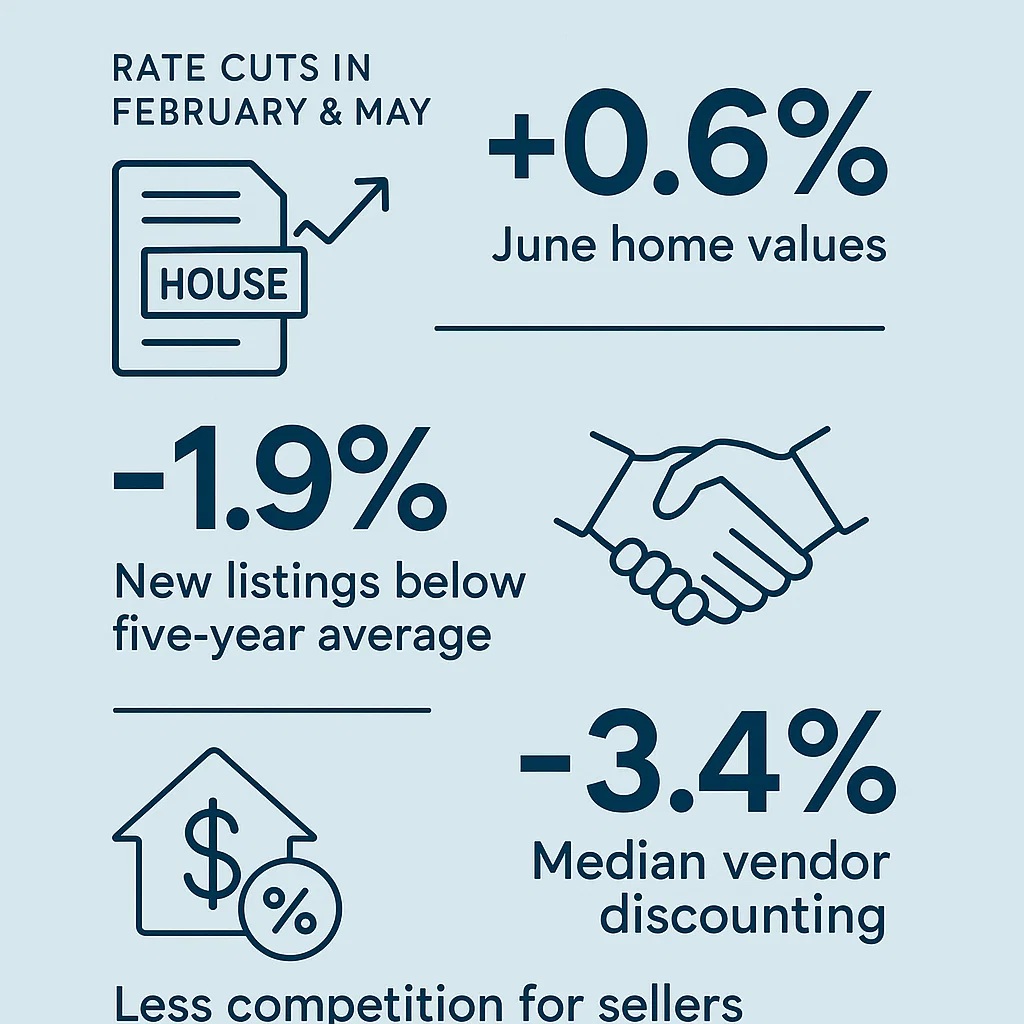

Despite the decision to hold, Australia's housing market remains robust. Thanks to earlier rate cuts in February and May, national home values increased by around 0.6% in June, marking five consecutive months of growth. New property listings are limited (around 1.9% below the five-year average), meaning less competition for sellers. Additionally, buyers are now offering closer to asking prices, reflected in median vendor discounting narrowing to -3.4% (based on CoreLogic data).

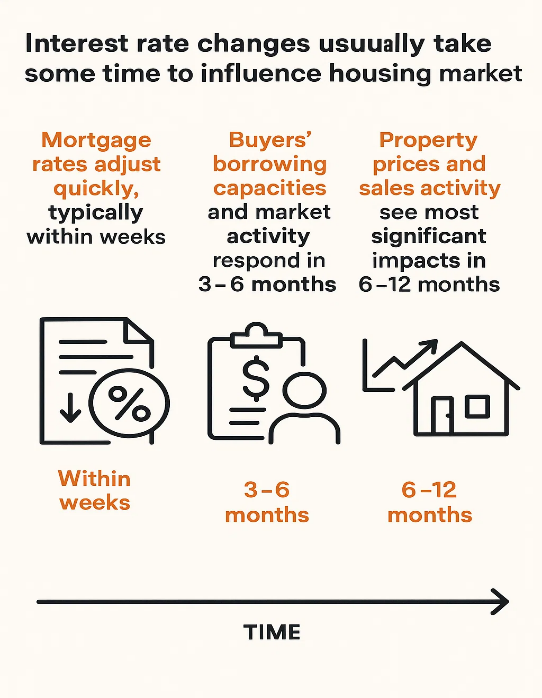

Interest rate changes usually take some time to influence the housing market fully. Mortgage rates adjust quickly, typically within days or weeks, but buyers’ borrowing capacities and overall market activity take around 3–6 months to respond. Property prices and sales activity typically experience their most significant impacts within 6–12 months following a rate adjustment. Consequently, if rates decrease (possibly as soon as August) homeowners can expect notable market benefits extending into early-to-mid 2026.

For homeowners considering selling, current market conditions are highly favourable. Mortgage rates remain stable, preserving potential buyers' purchasing power. Limited available homes continue driving strong buyer interest and reduced discounting. Well-priced and attractively presented homes are selling quickly.

Sellers aiming to maximise their returns should consider launching their sales campaigns in late July. This timing positions their homes to attract motivated buyers now, as well as those anticipating greater affordability from a potential rate cut in August. Additionally, a recent Domain survey found that homes featuring energy-efficient or climate-resilient improvements can attract price premiums of 4–6%.

Industry experts anticipate two to three more rate cuts later this year. If RBA cuts rates again by 0.25% in August, expect an increase in borrowing capacity by around A$9,000 per buyer. Such a move could further stimulate property prices, especially in areas with limited housing supply.

The bottom line: Although the RBA paused rates this month, interest rates are expected to continue to fall. The July decision has not slowed housing market momentum, maintaining favourable conditions for sellers. Keep an eye on upcoming key dates to stay informed and ready for the spring selling season.

Recent Posts

You might also like

RBA decision August 2025: What homeowners should know

August 15, 2025