Australia’s cash rate decisions are now made by a newly established nine-member Monetary Policy Board (MPB), replacing the former Reserve Bank Board. As this new structure settles into place, cash rate announcements have become somewhat less predictable, causing concern for some. However, there’s no need to worry if the decision doesn’t match what the markets were expecting. This uncertainty is temporary, and markets will quickly adapt as the new routine becomes familiar. For sellers, these changes can mean sudden shifts in enquiry levels, auction clearance rates, and buyer urgency.

What’s new and why it matters

Since March 2025, the Reserve Board of Australia (RBA) has made several changes to how interest rate decisions are made and shared. These include the formation of the MPB, adjustments to the Board’s meeting schedule, the timing and format of decision announcements, the release of meeting minutes, and the disclosure of vote splits. Table 1 below outlines these changes in more detail.

These adjustments have initially increased uncertainty, evidenced by a surprising decision in July to hold rates steady at 3.85% with a 6–3 vote split, followed by a unanimous 25 basis point cut to 3.60% in August, which was in line with market expectations. This is exactly the kind of teething-phase unpredictability that happens when decision styles and communications change. Market commentators have also linked the near-term unpredictability to the larger share of external members whose reaction functions are not yet well mapped.

RBA officials openly acknowledge this transitional phase. Deputy Governor Andrew Hauser explained clearly, “We’re feeling our way... it’s a board decision, not an individual decision.” A reminder that less forward guidance and more voices can mean the occasional misread while everyone learns the cadence.

How the new system works (at a glance)

Note: This table compares the previous Reserve Bank Board arrangements with the March changes. Source: Reserve Bank of Australia (RBA)

The ‘choppy’ phase won’t last forever

International experience shows clearly communicated central bank policies lead markets to quickly adapt. Australia's housing market historically aligns closely with the direction of interest rates, and this brief uncertainty is unlikely to change that trend.

This isn’t the first time the market has faced mixed signals. Between April and July 2023, it became harder for experts to predict what the RBA would do. In April, inflation data arrived later than usual and were higher than expected, leaving little time to adjust forecasts. The RBA then delivered surprise hikes in May and June, even as some indicators were softening. By July, economists were split in their views, and the RBA itself described the decision as “finely balanced”. Without a clear message from the Bank and with mixed signals in the data, the result was ongoing uncertainty in the lead-up to each meeting.

Despite the noise, markets gradually found their footing. After the RBA held rates steady in July, it used the post-meeting press conference to signal that it would “wait and see” the next inflation print before taking further action. When the June-quarter CPI landed within the target range (headline inflation at 2.1 percent and trimmed mean at 2.7 percent), most economists adjusted their outlook accordingly.

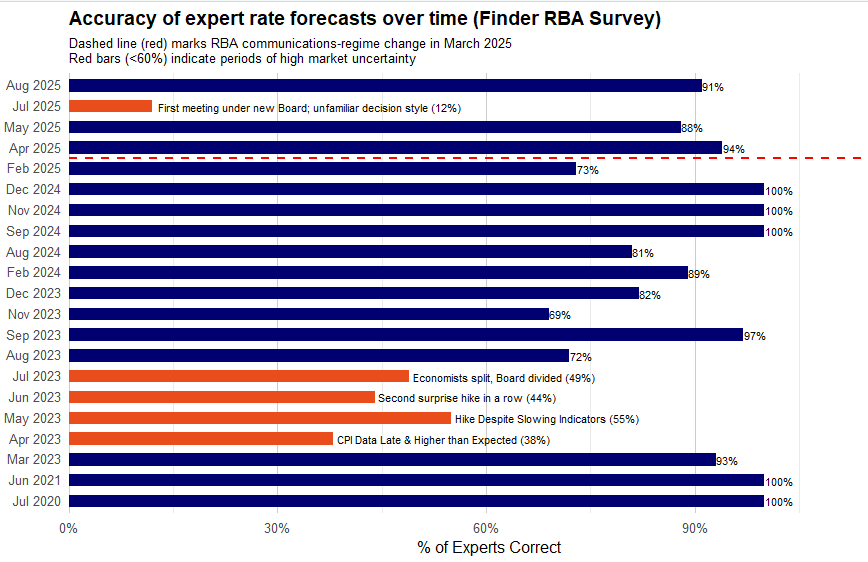

Note: Expert hit-rates on RBA decisions since 2020. Accuracy improves after 2025 communication reforms. Source: Finder RBA Cash Rate Survey (compiled by roomr).

The chart above from Finder’s RBA Survey shows this shift clearly (see Figure 1). While only 12 percent of experts correctly predicted the July hold, 91 percent forecast the August cut accurately, one of the sharpest month-to-month improvements in recent times. Many of the experts in the Survey explicitly pointed to the RBA’s “wait‑and‑see” approach and clear communication about incoming CPI data as key reasons why their improved accuracy. This reinforces the broader point: the more clearly the RBA communicates, the better markets become at forming accurate expectations.

Clearer RBA communication doesn’t just help economists; it benefits homeowners too. When markets have more certainty, buyers and sellers can make decisions with greater confidence. Dr. Alicia Bubb, Chief Economist at roomr, explains:

“Don't panic if a decision doesn't match initial market expectations. Early in a new framework, such mismatches are normal. The gap between expectations and outcomes will quickly close as everyone adjusts.”

What does this uncertainty mean for you?

When interest rate changes take the market by surprise, buyer and seller activity can shift quickly. Recognising these patterns can help you plan more effectively, especially when cuts are expected. Many Australian mortgages are variable and short-term fixed. This means cash-rate changes reach household budgets faster than in many other countries. Here is what you can typically expect:

- Variable Rates Adjust Quickly: Banks usually follow RBA decisions, though the timing and size of rate changes differ between lenders and loan products. Plan your campaign around when major lenders’ cuts take effect to take advantage of these changes.

- “Wait-and-see” behaviour shows up in enquiry and listings: Uncertainty can cause temporary hesitation among buyers and sellers. In July 2023, for example, national new listings fell 2.1% month-on-month and 4.9% year-on-year, with double-digit declines in some capitals (Perth –14%, Darwin –17%). If the decision or tone surprises, enquiries can dip for several days while markets and media adjust. Monitor local clearance rates and listings for timely insights, as these can lag RBA decisions by a week or more. Campaigns already underway are less affected in the short term, but changes in buyer behaviour often show up in later auction cycles.

What to Expect with Recent Cuts

This month’s cut was widely anticipated, giving buyers time to prepare (unlike the RBA’s surprise hold in July, which created a short wait-and-see period). We analysed that earlier hold, and how it set the stage for this cut, in our previous article [link]). So, what should you expect this time around? Here’s what’s likely to unfold in the market over the coming weeks:

- Increased Pre-approvals (and ready buyers): Anticipated cuts often prompt buyers to act early to secure finance. Loan Market reported a 30% rise in pre-approvals and loan applications ahead of predicted cuts in early 2025 compared with the prior year. Mortgage brokers also note an uptick in buyer enquiries, particularly from first home buyers, as confidence grows. For sellers, this means a larger pool of finance-ready bidders and, sometimes two waves of demand: one from proactive buyers before the cut and another after lenders pass it on. Use open homes to gauge buyer readiness and competition levels.

- Buyers have more borrowing power: A 25-basis-point cut typically reduces repayments by around $70–$80 per month per $500,000 borrowed, enough to lift borrowing capacity for some buyers. For a $900,000 loan, this equates to an extra $126–$144 in monthly budget, which can help some hesitant buyers become active bidders, particularly in competitive markets. Timing matters: pass-through is usually faster for variable-rate loans, but differences in pass-through speed mean the boost may be staggered across your campaign.

Bottom line

The RBA’s new way of setting and communicating rate decisions has created short bursts of heightened uncertainty, but for sellers, these moments can be used strategically. As the market adjusts to the new structure, predictability will improve, and interest rate trends will once again align with clear buyer signals.

If you’re selling, align your campaign with periods of strong buyer confidence and borrowing capacity. Cuts can create two phases of activity; an early lift from pre-approved buyers before the announcement and a second wave once lenders pass on the cut. Understanding and timing these phases can help you attract more bidders, shorten days on market, and achieve stronger offers, depending on local conditions and demand.

Stay informed, track lender pass-through timing, and work with your agent to launch when buyers are most finance-ready.

Prepare, plan, and position your property for the wave: don’t panic.

.jpg)